When comes to setting the criteria and requirements for a dream house, the list of considerations can definitely go on and on, from location to its’ proximity to the nearby MRT stations and amenities, to whether it is a freehold or leasehold property. However before getting to all these, do ensure that you are financially ready first.

Things to note before buying your dream house

Setting the Budget

With great property comes great responsibility, getting a new property is a long term financial commitment for the majority, it is important to be aware of one’s financial status well and not overstretch the working budget. Below are some of the financial considerations that one need to take note when setting a budget for the new home.

Cash Downpayment & Bank Loan Eligibility

Under the MAS regulation on Residential Property loan (w.ef 6th July 2018 ), the Loan To Value (LTV) Limit for an individual that has no existing loan is 75% or 55%. Meaning to say that the maximum loan amount one can borrow up to is 75% of the property price or 55% if the loan tenure is more than 30 years or extends past age 65 (subjected to borrower’s income and age). A minimum 5% and 10% cash down payment is required for LTV of 75% and 55% respectively.

Paying Via CPF

Yes, if you do not have any current property loan and is able to loan up to 75% of the property, you can pay the remaining 20% via your cpf ordinary account. But for existing property owner, do take note that you are required to set aside a minimum sum before you can utilise your cpf for your second property.

-

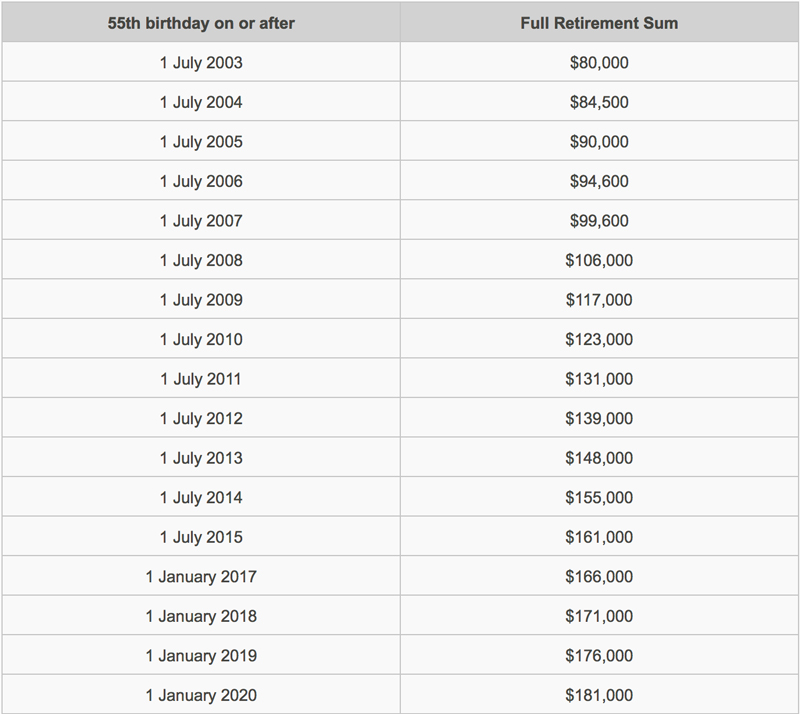

CPF Minimum Sum

For existing property owner who has utilised portion of the CPF to finance his/her existing property, HALF of the CPF full retirement sum is required to be kept in the CPF Special Account and/or CPF Ordinary Account (if there is insufficient fund in the Special Account). The CPF Basic Retirement Sum (used to be known as Minimum Sum) increases every year. Starting from 1st January 2019, the Basic Retirement Sum required is $88,000, which is half of $176, 000

Stamp Duty

Buyer's Stamp Duty (BSD)

| Based on the purchased price or market value, whichever is higher | |

|---|---|

| First $180,000 | 1% |

| Next $180,000 | 2% |

| Next $640,000 | 3% |

| Next $500,000 | 4% |

| Next $1,500,000 | 5% |

| Remaining | 6% |

Buyer Stamp Duty (BSD) is required for all Singapore Citizens, Singapore PR and Foreigners. You can use simple formulas below to calculate the BSD you are required to pay:

For a property purchased or valued (whichever is the higher amount) at $1 million and below,

3% x Purchase Price / Market Value of Property (whichever is the higher amount) – $5,400

For a property purchased or valued (whichever is the higher amount) above $1 million,

4% x Purchase Price / Market Value of Property (whichever is the higher amount) – $15,400

Additional Buyer's Stamp Duty (ABSD)

| Profile Of Buyer | ABSD rates: 6th July 2018 - 15th Dec 2021 | ABSD rates: 16th Dec 2021 - 26th Apr 2023 | ABSD rates: On or After 27th Apr 2023 |

|---|---|---|---|

| Singapore Citizen Buying First Residential Property | Nil | Nil | Nil (No Change) |

| Singapore Citizen Buying Second Residential Property | 12% | 17% | 20% (Revised) |

| Singapore Citizen Buying Third and subsequent Residential Property | 15% | 25% | 30% (Revised) |

| Singapore PR buying First Residential Property | 5% | 5% | 5% (No Change) |

| Singapore PR buying Second Residential Property | 15% | 25% | 30% (Revised) |

| Singapore PR buying Third and subsequent Residential Property | 15% | 30% | 35% (Revised) |

| Foreigners buying residential property | 20% | 30% | 60% (Revised) |

| Entities buying residential property | 25% Plus Additional 5% for Developers (Non-Remittable) | 35% Plus Additional 5% for Developers (Non-Remittable) | 35% Plus Additional 5% for Developers (Non-Remittable) |

Additional Buyer Stamp Duty (ABSD) is applicable to the above mentioned cases

Under the respective Free Trade Agreements (FTAs), Nationals or Permanent Residents of the following countries will be accorded the same Stamp Duty treatment as Singapore Citizens:

- Nationals and Permanent Residents of Iceland, Liechtenstein, Norway or Switzerland

- Nationals of the United States of America

Besides avoid leaving yourself financially strapped, it is important to take into considerations some other factors below as well,

MOP – Minimum Occupation Period

For existing HDB or Executive Condo (EC) owner, the 5-year Minimum Occupation Period must be met before making any new residential purchase. MOP starts from the date of possession of the flat / EC (key collection day).

New Launch or Resale

For new launch condo, the unit will only be ready upon TOP date which might take up to 4 years depending on the progress of the construction. For resale property, buyer will be able to get their units in about 8-10 weeks’ time.

For more information on this, a summary of this can be found by clicking our link here, New or Resale Homes.